A restaurant advertising jobs looks to attract workers in Oceanside, California, U.S., May 10, 2021. REUTERS/Mike Blake/

Register now for FREE unlimited access to Reuters.com

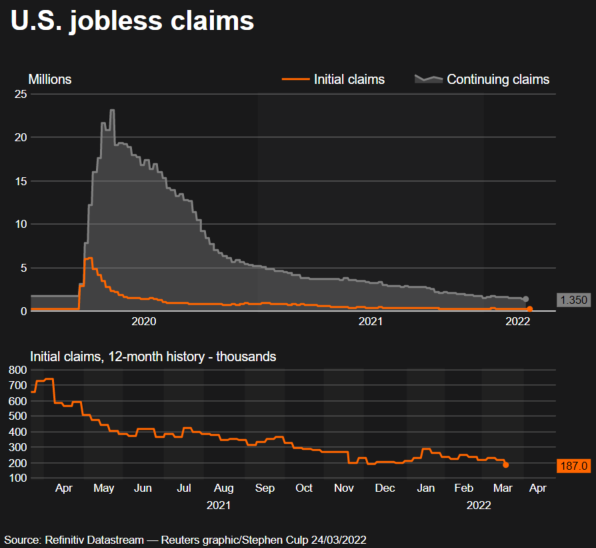

WASHINGTON, March 24 (Reuters) - The number of Americans filing new claims for jobless benefits dropped to a 52-1/2-year low last week, while unemployment rolls continued to shrink, pointing to rapidly diminishing labor market slack that will keep boosting wage inflation.

The strength in the job market reported by the Labor Department on Thursday may push the Federal Reserve to raise interest rates by half a percentage point at its next policy meeting in May. Fed Chair Jerome Powell on Monday said the U.S. central bank must move "expeditiously" to raise rates and possibly "more aggressively" to keep high inflation from becoming entrenched. read more

The Fed last week increased its policy interest rate by 25 basis points, the first hike in more than three years.

Register now for FREE unlimited access to Reuters.com

"U.S. businesses are not laying off workers because they know the enormous challenges they're facing in filling open positions," said Ryan Sweet, a senior economist at Moody's Analytics in West Chester, Pennsylvania.

"If initial claims remain below 200,000 for a period of time, it will raise a red flag with the Fed."

Initial claims for state unemployment benefits fell 28,000 to a seasonally adjusted 187,000 for the week ended March 19, the lowest level since September 1969. Economists polled by Reuters had forecast 212,000 applications for the latest week.

Last week's drop in claims was widespread, with large decreases in California, Michigan, Kentucky and Illinois.

Claims have been declining in part as COVID-19 restrictions across the country have been lifted amid a massive drop in coronavirus cases. They have plunged from a record high of 6.149 million in early April 2020.

There are no signs that Russia's war against Ukraine, which has sent U.S. gasoline prices to record highs and is expected to worsen the strain on global supply chains, has impacted the labor market and business activity.

A survey from S&P Global on Thursday showed its flash U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, rose to an eight-month high of 58.5 in March from 55.9 in February,fueled by strong demand for both goods and services. Businesses were upbeat about the outlook this year, but services firms worried about the fallout from the rising cost of living caused by the Russia-Ukraine war.

Stocks on Wall Street rebounded from a sharp drop on Wednesday. The dollar (.DXY) edged up against a basket of currencies. Prices of U.S. Treasuries fell.

STRONG BUSINESS INVESTMENT

A third report from the Commerce Department showed orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, fell 0.3% in February, the first decline in a year. But data for January was revised higher to show these so-called core capital goods orders accelerating 1.3% instead of 1.0% as previously reported.

Last month's drop reflected decreases in orders for machinery, primary metals, fabricated metals as well as computers and electronic products.

Shipments of core capital goods gained 0.5% last month. Data for January was also revised up to show shipments increasing 2.1% in January instead of the previously estimated 1.9%.

Core capital goods shipments are used to calculate equipment spending in the gross domestic product measurement. Given January's revision, economists expect strong business investment in equipment this quarter.

"It is possible that the February declines represent a shift in businesses' intentions for capex, but the February figures also may just reflect noise in the monthly data," said Daniel Silver, an economist at JPMorgan in New York. "We think real equipment spending is on track for strong growth in the first quarter even with related price increases offsetting some of the nominal gains."

Layoffs are likely to remain low for some time amid an acute shortage of workers. There were 11.3 million job openings at the end of January, with a record 1.8 open positions per unemployed person. This misalignment between demand for labor and supply is boosting wage growth, which is providing some cushion to households against the soaring gasoline prices, as well as feeding into high inflation.

More people could rejoin the workforce this month as COVID-19 infections tumble, which would boost payrolls growth.

The claims report showed the number of people receiving benefits after an initial week of aid decreased 67,000 to 1.350 million during the week ended March 12, the lowest since January, 1970. The so-called continued claims data covered the period during which the government surveyed households for March's unemployment rate.

Continued claims declined sharply between the February and March survey periods. The unemployment rate fell to a two-year low of 3.8% in February.

"These data suggest that the March employment situation report is likely to be similar to recent reports, which have shown strong job growth and continuing declines in the unemployment rate," said Conrad DeQuadros, senior economic advisor at Brean Capital in New York.

Register now for FREE unlimited access to Reuters.com

Reporting by Lucia Mutikani Editing by Chizu Nomiyama and Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

Business - Latest - Google News

March 24, 2022 at 10:56PM

https://ift.tt/OIhXV36

U.S. labor market tightens as weekly jobless claims hit lowest level since 1969 - Reuters

Business - Latest - Google News

https://ift.tt/QBPi8aO

Bagikan Berita Ini

0 Response to "U.S. labor market tightens as weekly jobless claims hit lowest level since 1969 - Reuters"

Post a Comment